Information you will need to get together in order to talk to a lender regarding a pre-approval.

HERE’S HOW TO GET READY.

Knowing how much home you can afford saves you time, and tells sellers you’re serious about buying a home. Here is a list of information you will need in order to get a free loan pre-approval decision. (you can email me and I can send you a list of lenders or you can ask at your bank or financial institution)

Personal Information:

* The name, address and Social Security number of each person applying for the loan.

* The name, address and phone number of your current landlord or mortgage company, if applicable.

Assets:

* The source(s) of funds for your down payment and closing costs.

* Your bank name and approximate balance of your checking and savings accounts.

* The value of any stocks, bonds, mutual funds or other assets you own.

* Net worth of business owned, if applicable.

Income:

* Your gross monthly income (list salary base, commission and bonuses separately)

* Employment information, including company, address, phone number and dates of employment for two years.

* Other income, including child support or alimony, Social Security, retirement, dividend or interest income.

Liabilities:

* Credit cards and installment loans.

* Information about any other properties you own, including rentals, second home and investment properties.

* Alimony and/or child support payments, if applicable.

If you have all this information together prior to contacting your lender for a pre-approval – the pre-approval process should go smoothly and quickly.

Here are some helpful “Do’s and Don’ts”

when applying for a mortgage…

DO’S !

Keep originals or be able to access on your employer/bank sites all pay-stubs, bank statements and other important financial documents.

Provide your Earnest Money Deposit from your own personal bank account or acceptable gift funds. Please talk to your Loan Consultant for additional clarification. This will present a very difficult problem if not managed properly in the beginning.

Provide all documentation for the sale of your current home, including sales contract, closing statement, employer relocation/buy-out program if applicable.

Notify your Loan Consultant if you plan to receive gift funds for closing. Gift funds are acceptable only if certain criteria are met. Advances from credit cards for down payment/closing costs are never acceptable.

Notify your Loan Consultant of any employment changes such as recent raise, promotion, transfer, change of pay status, for example, salary to commission.

Be aware that a new credit report could be pulled just prior to closing.

DON’T !

Close or open any asset accounts or transfer funds between accounts without asking your Loan Consultant about the proper documentation required for your loan. For example, before transferring all funds from your savings to your checking, check with your Loan Consultant.

Deposit any monies outside of your automated payroll deposits, particularly cash or sale of personal property, without notifying your Loan Consultant. Many guidelines require substantial documentation as to the source of these deposits.

Change jobs/employer without inquiring about the impact this change might have on your loan.

Make major purchases prior to or during closing such as new car, furniture, appliances, etc. as this may impact your qualifying amount.

Open or increase any liabilities, including credit cards, student loans or other lines of credit during the loan process as it may impact your qualifying amount.

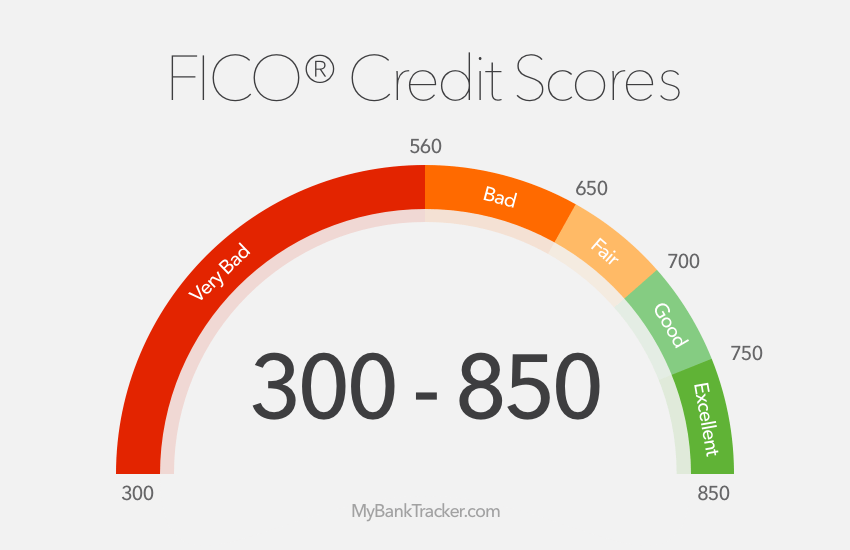

Understanding your Credit Score:

Your “Credit Score” is a number that reflects the information in your Credit Report.

Your “Credit Report” is a record of your credit history. It includes information about whether you pay your bills on time and how much you owe to creditors.

Your Credit Score can change, depending on how your credit history changes.

Your Credit Score can affect whether you can get a loan or mortgage and how much you will have to pay for that loan.

Scores range from a low of 450, to a high of 850.

Generally , the higher your score, the more likely you are to be offered better credit terms.

Click Here: 10 Things that Affect your Credit Score

What if there are mistakes in your credit report?

You have a right to dispute any inaccurate information in your Credit Report. If you find mistakes on your Credit Report, contact the consumer reporting agency. It is a good idea to check your Credit Report to make sure the information it contains is accurate.

How can I get my free annual Credit Report?

Under federal law, you have the right to obtain a FREE copy of your Credit Report from each of the nationwide consumer reporting agencies once a year.

To Obtain your FREE Annual Copy of your credit report:

By Telephone: Call toll-free: 1-877-322-8228

On the Web: Visit www.annualcreditreport.com secure link to site – click here

By Mail: Mail your completed Annual Credit Report Request Form – which you can obtain by clicking:

****************

{kind=link}